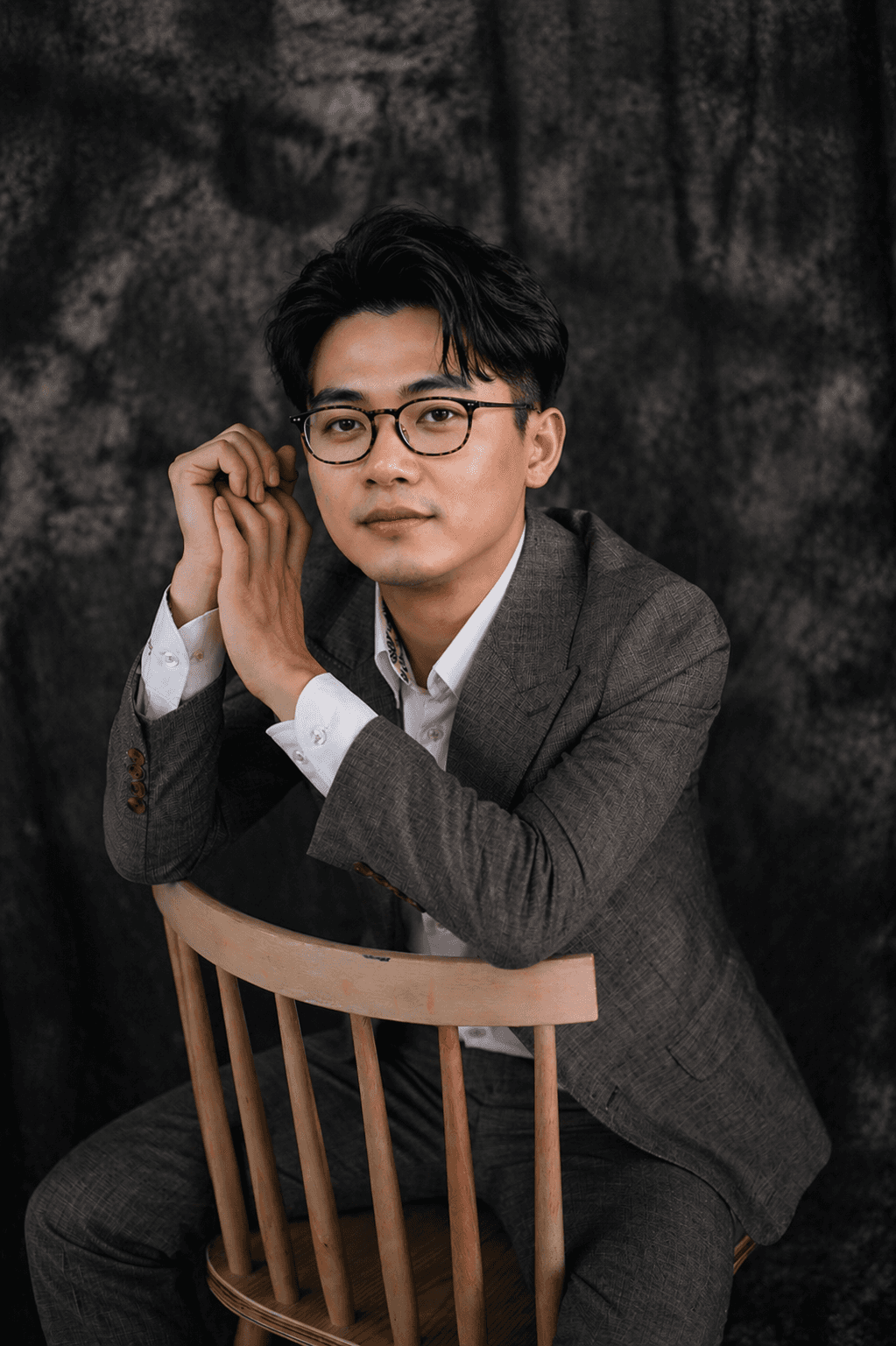

Dr. Ethan Zhao

Research Lead

PhD in machine learning from Tsinghua. Runs the model layer — pattern detection and predictive systems across timeframes. Previously led an AI research team developing quantitative trading algorithms with multi-year live performance.